You Are Not Losing to Competitors. You Are Competing in the Wrong Ocean.

- Felipe Afanador Cortés

- Mar 12

- 6 min read

Key Takeaways

Map your current strategic canvas before designing a new one. The visual convergence of competing firms is a diagnostic signal — it reveals the dimensions of the red ocean and identifies where differentiation is possible, absent, or obsolete.

Apply the ERRC grid as a diagnostic tool, not a brainstorming exercise. Eliminate and reduce before you raise and create. Structural Blue Ocean moves typically reduce complexity while raising the dimensions that generate genuine willingness to pay.

Blue Ocean thinking is not the absence of analysis — it is analysis in service of imagination. The firms that create new market spaces combine deep understanding of their value chain and activity structure with the courage to reframe what value means for an under-served or non-consuming customer.

Every year, thousands of strategy sessions across Latin America produce the same diagnosis: our competitors are gaining ground, our margins are under pressure, and we need to grow. The prescription that usually follows is equally predictable — invest more in sales, sharpen the product, cut costs, and differentiate. It is advice that is analytically coherent and practically exhausting. The reason is simple: when an entire industry competes along the same set of attributes, improving performance on those dimensions generates incremental returns, not transformation. This is what W. Chan Kim and Renée Mauborgne called a red ocean — a contested market space where boundaries are fixed and value is divided, not created.

The diagnosis matters more than we tend to admit. In their foundational work on competitive advantage, Pankaj Ghemawat and Jan W. Rivkin established that a firm creates value only when it widens the wedge between what customers are willing to pay and what it costs to serve them — and only when that wedge is wider than what rivals can achieve. The insight is deceptively simple: you cannot capture value you have not first created. Yet most organizations direct their strategic energy at capturing a larger share of an existing wedge rather than engineering a fundamentally larger one. They compete for the same customers, using the same variables, in the same logic of value. The ocean turns red not because the strategy is wrong in isolation — it is because everyone is executing a version of the same strategy simultaneously.

The question is not how to beat the competition. It is how to make the competition irrelevant.

Blue Ocean Strategy proposes a structural reorientation. Rather than asking "how do we perform better on the attributes the industry competes on?", it asks "which attributes should we eliminate, reduce, raise, or create?" The four-action framework at its core is a diagnostic instrument, not a brainstorming exercise. It forces leaders to interrogate the assumptions embedded in their current value proposition — assumptions often so internalized that they are no longer visible as choices. In the consulting industry across LATAM, for instance, most firms compete on the same variables: industry expertise, senior team credentials, geographic coverage, and price. The strategic canvas of a typical consulting firm looks remarkably similar to that of its closest rival. That convergence is not a coincidence. It is a symptom of red ocean thinking.

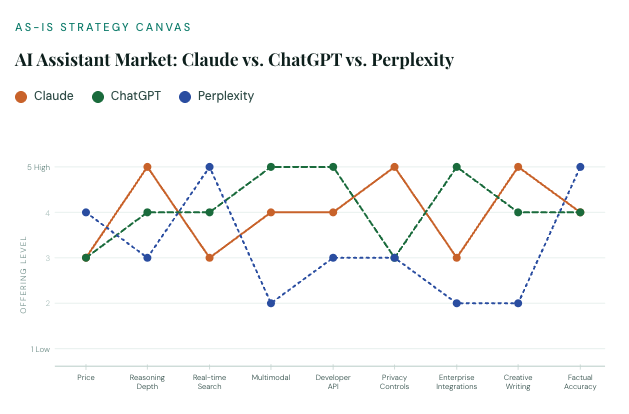

To make this visible and actionable, consider a concrete example from the AI assistant market — one of the most competitive digital spaces in the world today. Claude, ChatGPT, and Perplexity currently compete across a set of well-defined variables: subscription price, depth of reasoning, real-time web search, multimodal capabilities, developer API access, privacy controls, enterprise integrations, creative writing quality, and factual accuracy. Below is the strategy canvas for this competitive landscape.

As-Is Strategy Canvas

Ratings represent qualitative competitive positioning (1–5 scale) based on publicly available features as of early 2025. Hover over any data point to explore. Higher score = stronger offering on that dimension. "Price" is rated inversely — a higher score reflects more accessible or generous free-tier pricing.

What does the canvas reveal? Three players. Nine variables. And, critically, a striking convergence on several axes — price, developer API, and factual accuracy are the arenas where all three compete intensely and earn similar scores. This visual pattern is the hallmark of a red ocean: the more similar the curves, the more commoditized the competition. Ghemawat and Rivkin's framework would call this the erosion of added value — when a competitor can replicate your position, your ability to capture value diminishes. In the AI assistant space, the result is a relentless feature arms race, a price war on premium tiers, and a customer experience that feels increasingly interchangeable.

But the canvas also shows something more interesting: the divergences. Perplexity scores exceptionally high on real-time search and factual accuracy while scoring low on creative writing, enterprise integrations, and multimodal capabilities. Claude leads on reasoning depth, privacy controls, and creative writing but trails on enterprise integrations. ChatGPT dominates on multimodal and enterprise reach. These asymmetries are not accidents — they reflect deliberate strategic trade-offs. And it is precisely in those trade-offs that Blue Ocean opportunity hides. An entrant that radically eliminates price friction, raises contextual reasoning, and creates a new variable — say, industry-vertical specialization or autonomous workflow design — would not be competing on the existing canvas. It would be drawing a new one.

The most dangerous strategic assumption is that the current set of competing variables is fixed. It is not. It is a historical accident.

This is what Kim and Mauborgne's ERRC grid makes operational: Eliminate the factors the industry takes for granted but that add cost without generating meaningful willingness to pay. Reduce those that are over-engineered relative to what buyers actually value. Raise those that are systematically undervalued. And create dimensions of value that the industry has never considered. The process is analytical and creative simultaneously. It requires what Ghemawat and Rivkin describe as activity analysis — the systematic decomposition of a firm's value chain to understand which activities drive cost and which drive willingness to pay — combined with the imagination to envision a different configuration entirely.

The ERRC logic applied to the AI canvas

Ahypothetical Blue Ocean entrant in the AI assistant space might eliminate complex pricing tiers that confuse buyers, reduce emphasis on general multimodal features that most users rarely activate, raise deep domain specialization and audit-grade output traceability, and create a new variable — proactive workflow orchestration — that none of the current players have made central to their value proposition. The resulting strategy canvas would look fundamentally different from Claude's, ChatGPT's, or Perplexity's. That differentiation is not decorative. It is structural.

In Latin American markets, this logic is particularly urgent. Most medium-sized companies operate in industries where the competitive canvas has not been redrawn in a decade. Retail banking, insurance, professional services, logistics — these are sectors where the incumbents compete on the same four or five variables they have always competed on, and where new entrants can create blue oceans not by matching incumbents on their strengths but by rendering entire categories of competition irrelevant. The consulting firms that trained 50 executives in "AI awareness" are competing in the same ocean as the firms that trained 500. The firms that redesign the decision-making architecture of their clients — embedding intelligence into workflows, reconfiguring how strategic choices are made — are swimming in a different body of water entirely.

It is worth being honest about the limits of this framework. Blue Ocean Strategy is not a formula. As Ghemawat and Rivkin noted in their analysis of competitive advantage, many of the greatest advantages come not from structured analysis but from insight, experimentation, and trial and error. The strategy canvas is a map, not a compass. It shows you where the industry is. It does not automatically reveal where to go. That leap requires what no framework can fully encode: the capacity to observe customer frustrations that buyers themselves have not yet articulated, to imagine the constraints that could be removed, and to build an organization capable of executing a fundamentally different set of choices in unison.

Growth, then, is not primarily a sales problem or a marketing problem. It is a strategic imagination problem. The question is not how to grow within the existing rules of competition. It is how to rewrite them. That requires leaders who are willing to stop optimizing the current canvas and start designing the next one — with the analytical discipline to understand why the wedge between willingness to pay and cost looks the way it does today, and the creative vision to engineer a wider one tomorrow.

Comments